Categories

Latest Post

Making Tax Digital Checklist 2026

MTD Quarterly Updates 2026

MTD Qualifying Income Explained 2026

Making Tax Digital Penalties 2026

Have Any Question?

If you have any questions about our services, call us or email at:

- +44 75 079 66252

- contact@mtd-makingtaxdigital.co.uk

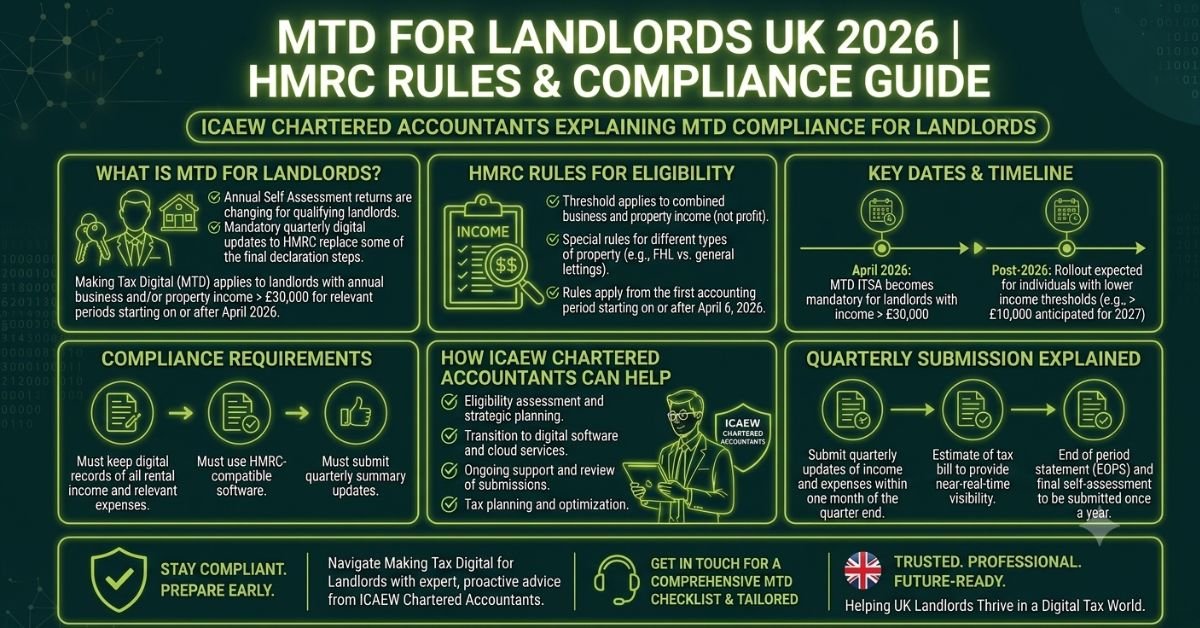

MTD for Landlords UK 2026 | HMRC Rules & Compliance Guide

If you’re a UK landlord with rental income, Making Tax Digital (MTD) is the biggest tax compliance shake-up you’ll face in 2026. From 6 April 2026, landlords earning over £50,000 from rental properties (and any self-employment) will be legally required to keep digital records and submit tax updates to HMRC every quarter, replacing the once-a-year self-assessment.

The thresholds drop in 2027 (£30,000) and 2028 (£20,000), meaning almost every UK landlord will be affected within 3 years.

This guide is written by ICAEW chartered accountants for UK landlords, buy-to-let owners, HMO landlords, holiday-let owners, accidental landlords, and non-resident landlords. We’ll cover every HMRC rule, deadline, threshold, penalty, and the exact steps to get your rental business MTD-ready.

Let’s start with what HMRC actually requires.

What Are HMRC’s MTD Rules for Landlords?

Under HMRC’s Making Tax Digital for Income Tax Self-Assessment (MTD ITSA), every UK landlord meeting the threshold must:

- Keep digital records of all rental income and property expenses in MTD-compatible software

- Submit 4 quarterly updates to HMRC per tax year via approved software

- File a Final Declaration at year-end (replacing the old self-assessment return)

- Maintain digital links between any software you use (no copying and pasting between Excel and accounting tools)

In simple terms, HMRC wants real-time visibility of your rental income and expenses, not just an annual summary in January.

Important: MTD doesn’t change how landlords are taxed (Section 24 mortgage interest restriction, capital allowances, allowable expenses, all stay the same). It only changes HOW you report. But quarterly submission means HMRC’s algorithms can spot discrepancies much faster than under the old annual system.

Which UK Landlords Are Affected by MTD?

MTD ITSA applies to UK landlords whose qualifying income (rental + any self-employment) exceeds the threshold for their tax year:

Tax Year Starting | Qualifying Income Threshold | Landlords Affected |

|---|---|---|

6 April 2026 | Over £50,000 | Large portfolio landlords, HMO operators, holiday-let owners |

6 April 2027 | Over £30,000 | Mid-tier landlords with 2-3 properties |

6 April 2028 | Over £20,000 | Most UK landlords, including small portfolios |

Critical point: Once you cross the threshold once, you stay in MTD ITSA for a minimum of 3 years — even if your rental income drops below the threshold in later years. Don’t assume “I’ll just stay under the limit.”

Which Types of UK Landlords Must Comply?

- Buy-to-let landlords – traditional residential rental property owners

- HMO landlords – houses in multiple occupation (high-yield, more complex tax)

- Holiday let owners – Airbnb hosts, Furnished Holiday Lets (FHL) — note FHL tax status changed in April 2025

- Portfolio landlords – anyone with 4+ rental properties

- Accidental landlords – people renting out their previous home

- Student property landlords – letting near universities, often high turnover

- Commercial property landlords – if income exceeds threshold (different rules to residential, but MTD still applies)

- Non-resident landlords – overseas-based owners of UK property (NRL scheme separately, but MTD applies if threshold met)

- Furnished and unfurnished landlords – both types are equally affected

Read our detailed guide for Non-Resident Landlords & MTD if you live abroad but own UK property.

What Counts as Qualifying Rental Income for MTD?

This is where many landlords get confused. HMRC uses gross rental income (not net profit) to assess the MTD threshold.

Counts Toward MTD Threshold:

- Gross rent received from UK residential property

- Gross rent from UK commercial property

- Holiday let / FHL income

- Furnished room rent (Rent-a-Room scheme above £7,500/year threshold)

- Overseas property income (if UK-resident landlord)

- Service charges and ground rent received

- Income from licensing rooms (HMO tenants)

Does NOT Count Toward MTD Threshold:

- PAYE salary or employment income

- Dividends from your own limited company

- Interest income

- Pension income

- Capital gains from property sales

- Rent below the £1,000 property allowance

Real Example; James, Manchester Buy-to-Let Landlord

Income Source | Annual Amount | Counts Toward MTD Threshold? |

|---|---|---|

Rent from 3 BTL properties in Manchester | £36,000 (gross) |

|

Income from 1 HMO (5 tenants) | £24,000 (gross) |

|

His PAYE salary (full-time job) | £42,000 |

|

Dividend from ISA investments | £1,200 |

|

TOTAL QUALIFYING RENTAL INCOME | £60,000 |

|

Yes — counts in full

Yes — counts in full No — PAYE excluded

No — PAYE excludedJames’s qualifying income is £60,000, well over the £50,000 threshold. He must comply with MTD ITSA from 6 April 2026 even though his “profit” after mortgage interest, maintenance, and management fees is much lower.

Common mistake: Landlords often think the threshold is based on profit. It’s not, it’s based on GROSS rent. A landlord with £40,000 in rent and £30,000 in expenses (so £10,000 profit) still has £40,000 of qualifying income.

Read our complete MTD Qualifying Income guide for more landlord-specific examples.

MTD Deadlines for Landlords (2026-2028)

Once you’re in MTD ITSA, you’ll submit 4 quarterly updates per tax year plus a Final Declaration:

Quarter | Period Covered | Filing Deadline |

|---|---|---|

Q1 | 6 April – 5 July | 7 August |

Q2 | 6 July – 5 October | 7 November |

Q3 | 6 October – 5 January | 7 February |

Q4 | 6 January – 5 April | 7 May |

Final Declaration | Full tax year reconciliation | 31 January (following year) |

Each quarterly submission is cumulative — it includes income and expenses from the start of the tax year, not just the most recent 3 months.

See our full MTD Deadlines & Key Dates 2026 guide for every date through 2028.

Allowable Landlord Expenses Under MTD (What You Can Deduct)

MTD doesn’t change what you can claim, but you must record every expense digitally throughout the year. Here are the main categories of allowable landlord expenses:

Fully Allowable Expenses

Expense Category | Examples |

|---|---|

Letting agent fees | Tenant finding, ongoing management fees, marketing |

Repairs & maintenance | Boiler repairs, decorating, leak fixes (not improvements) |

Insurance | Landlord insurance, building insurance, rent guarantee |

Utility bills (if you pay) | Electricity, gas, water, council tax during void |

Ground rent & service charges | Leasehold property costs |

Accountancy & legal fees | Tax accountant, eviction solicitor |

Professional services | Gas safety certificates, EPC, EICR inspections |

Cleaning between tenants | End-of-tenancy cleaning, gardening |

Advertising | Rightmove, Zoopla, OpenRent listing fees |

Travel to property | Mileage for inspections (45p/mile rules apply) |

Restricted or Disallowable

- Mortgage interest; restricted to basic rate tax relief (20%) under Section 24 since April 2020

- Capital improvements; extensions, new kitchens, conservatories (these reduce CGT, not income tax)

- Personal use of property; periods when you stayed there yourself

- Replacement of “Domestic Items Relief”; only for replacements, not improvements

Pro tip from a chartered accountant: Under MTD’s quarterly visibility, HMRC’s algorithms can spot patterns like “large repair claims clustered at year-end” or “inconsistent expense ratios.” Keep your records clean, dated, and digitally linked from day one.

Best MTD Software for UK Landlords

Landlords have specific software needs, multiple properties, multiple tenants, deposit tracking, and clear separation between properties. Here’s how the main MTD options stack up:

|

Software |

Best For |

Approx Cost |

Landlord-Friendly Features |

|---|---|---|---|

|

Xero |

Portfolio landlords (4+ properties) |

£15-£35/mo |

Class-based tracking by property, multi-currency for overseas |

|

Hammock |

Dedicated landlord software |

£15-£30/mo |

Built specifically for UK landlords, property-by-property |

|

QuickBooks |

Smaller landlords (1-3 properties) |

£10-£25/mo |

Customer/job tracking by property |

|

FreeAgent |

NatWest/RBS landlords |

Free or £15/mo |

Simple, free if you bank with NatWest |

|

Excel + Bridging |

DIY landlords on tight budgets |

£0-£5/mo |

Free spreadsheet + bridging software like 123Sheets |

See our full comparison: Best MTD Software UK 2026, we benchmark each one specifically for landlord setups.

Our chartered accountant recommendation: For most UK landlords with 2-5 properties, Hammock or Xero (with property tracking) work best. For 6+ properties, only Xero scales properly. We help all our landlord clients set up the right tool, and we manage it for them.

MTD Penalties for Landlords: What You Risk

HMRC has set up a tougher penalty regime specifically for MTD. Here’s what you face as a landlord:

Failure | Penalty |

|---|---|

Missing 4 quarterly submissions (1 tax year) | £200 fine + 4 penalty points |

Late payment 16-30 days | 3% of tax owed (rising to 4% from April 2027) |

Late payment 31+ days | Additional 3% + 10% annual daily interest |

Not using MTD-compatible software | £400 per non-compliant return |

Failing to keep digital records | Up to £3,000 per failure |

No digital links between systems | Up to £3,000 per failure |

Real-world risk: A 4-property landlord who misses a year of quarterly MTD submissions could face £200 fine + £3,000 digital records penalty + late payment charges = £3,000+ in extra costs on top of the tax owed. Compliance is dramatically cheaper than non-compliance.

Read the full MTD Penalties guide for every penalty scenario.

Special Cases: Joint Landlords, Non-Residents & Property Companies

Joint Property Owners (Couples & Family Co-Owners)

If you own a property jointly (most commonly with a spouse or partner), each owner reports their share of the rental income separately. The MTD threshold applies to each individual’s qualifying income, not the property as a whole.

Tax planning tip: For married couples, joint ownership splits rental income proportionally (default 50/50 unless declared otherwise via Form 17). This can keep both partners under the MTD threshold longer, and reduce overall tax via the lower-earning spouse. A chartered accountant can structure this properly.

Non-Resident Landlords (NRL Scheme + MTD)

If you live abroad but own UK property, you’re under the Non-Resident Landlord (NRL) Scheme. Under NRL, your letting agent or tenant withholds basic-rate tax unless you have an NRL1 approval.

MTD applies in addition to NRL, if your UK rental income exceeds the threshold. Many overseas landlords miss this and end up double-penalised.

Read our detailed guide for Non-Resident Landlords & MTD for the full rules.

Property Owned Through a Limited Company

If you’ve incorporated your portfolio into a Special Purpose Vehicle (SPV) limited company, you’re NOT in MTD ITSA, you’re in Corporation Tax. MTD for Corporation Tax is expected from April 2027, with similar quarterly reporting requirements.

Furnished Holiday Lets (FHL), Major Change April 2025

The Furnished Holiday Let tax regime was abolished from April 2025. Holiday let income now counts as standard rental income for MTD purposes. If you have Airbnb income or run a holiday let, your gross income counts toward the £50k MTD threshold from April 2026.

Rent-a-Room Scheme

If you rent rooms in your own home, you can earn up to £7,500/year tax-free under the Rent-a-Room scheme. Income below this is exempt and doesn’t count toward MTD. Income above £7,500/year does count and must be reported.

How Landlords Can Get MTD-Ready: 8-Step Action Plan

Here’s the exact roadmap we use with our landlord clients to be fully MTD-ready by April 2026:

Step 1: Calculate Your Qualifying Rental Income

Add up the GROSS rent across all your UK and overseas property for the past 12 months. Include any service charges or licence fees received. If you’re over £50k, you’re in scope from April 2026.

Step 2: Set Up Property-Level Tracking

HMRC will want to see income and expenses per property, not just totals. Start labelling your bank account transactions by property NOW, even if you’re still using paper or basic spreadsheets.

Step 3: Open a Separate Landlord Bank Account

If you mix rental income with personal money, untangling 12 months of transactions before MTD launch is painful. Open a dedicated landlord account (Starling Business, Tide, Revolut Business — all free options) and route all rental income/expenses through it.

Step 4: Choose MTD-Compatible Software

Pick software that supports property-level tracking. Hammock, Xero (with classes), or QuickBooks (with customers/jobs) all work.

Step 5: Digitise Existing Records

Scan or photograph existing rental receipts, contracts, insurance docs, EPCs, gas safety certificates. Upload them to your accounting software’s document storage.

Step 6: Register with HMRC for MTD ITSA

You can register via your Government Gateway account, or have your accountant do it.

Step 7: Run a Practice Quarter (Highly Recommended)

Before MTD goes live in April 2026, simulate a quarterly submission with your existing data. Find the gaps now, not when penalties are at stake.

Step 8: Decide — DIY or Outsource?

Landlords with 1-2 properties may DIY successfully. Landlords with 3+ properties, HMOs, holiday lets, joint ownership, or non-resident status almost always benefit from chartered accountant MTD support. The complexity and risk justify the cost.

Download our free MTD Checklist (printable PDF) to track your progress.

5 Biggest MTD Mistakes Landlords Make

Mistake 1: Thinking “Rental Income Isn’t Self-Employment”

Many landlords assume MTD only applies to self-employed people. Wrong. MTD ITSA applies equally to property income, landlords are explicitly named in HMRC’s MTD rules.

Mistake 2: Mixing Properties in One “Pot”

Lumping all rental income into one figure makes quarterly submissions harder and audit risk higher. Always track by individual property, both income and expenses.

Mistake 3: Forgetting Section 24 Mortgage Interest Rules

Mortgage interest is no longer a deductible expense, it’s a 20% tax credit. Under MTD’s quarterly visibility, misclassifying mortgage interest as an expense will trigger HMRC’s algorithms much faster than under annual returns.

Mistake 4: Not Including Overseas Property

If you’re UK-resident and own property abroad, that overseas rental income counts toward your MTD threshold. Many landlords forget this and end up retroactively non-compliant.

Mistake 5: Treating MTD as Just “More Admin”

MTD is also an opportunity, quarterly visibility means you can spot tax planning opportunities throughout the year (not just in January), structure ownership smarter, and avoid surprise tax bills. The landlords who treat MTD as a tax planning tool win.

Real Case Study: How We Saved a 4-Property Landlord £7,000+

A Milton Keynes-based landlord came to us facing an HMRC enquiry into 5 years of his tax returns. He owned 4 BTL properties plus had self-employment income on the side. Like many landlords, he had been managing his own tax via spreadsheets and basic accounting software.

HMRC’s proposed additional tax liability + penalties was over £15,000.

What we did:

- Audited 5 years of property income across all 4 BTLs

- Reclassified expenses correctly (some were wrongly disallowed, others wrongly claimed)

- Identified overlooked reliefs — Replacement of Domestic Items Relief, repairs vs improvements distinction

- Built a formal appeal challenging HMRC’s penalty calculation

- Negotiated a settlement that reduced his liability significantly

Outcome: All HMRC penalties and fines waived. Tax liability reduced by over £7,000. Total saving vs HMRC’s original assessment: over £14,000.

Lesson for landlords: Under MTD’s quarterly visibility, these enquiries will become more common. Getting your records right from day one with chartered accountant support is far cheaper than fighting an HMRC enquiry later.

MTD for Landlords: Frequently Asked Questions

Do all landlords need to use Making Tax Digital?

Not yet, only landlords whose qualifying income exceeds the threshold for that tax year. £50,000 from April 2026, £30,000 from April 2027, and £20,000 from April 2028. Eventually, most UK landlords will be in scope.

What is the MTD threshold for landlords?

Based on gross qualifying income (rental + self-employment combined, before expenses): £50k from April 2026, £30k from April 2027, £20k from April 2028.

Do I need to register with HMRC for MTD as a landlord?

Yes, once your qualifying income exceeds the threshold, you must register before the start of that tax year. You can do this via your Government Gateway account or through your accountant.

Does rental income count toward MTD if I have a job too?

Only your gross rental income (plus self-employment) counts toward the MTD threshold. PAYE salary doesn’t count. But if your rental income alone exceeds the threshold, you’re in scope.

What MTD software is best for landlords?

For 1-2 properties: QuickBooks or FreeAgent. For 3-5 properties: Xero with property tracking or Hammock (purpose-built for UK landlords). For larger portfolios: Xero with proper class-based reporting.

Can I use a spreadsheet for MTD as a landlord?

Yes, but only if your Excel is connected to HMRC-approved bridging software (like 123Sheets or VitalTax). Sending a standalone spreadsheet to HMRC is not MTD-compliant.

How often do landlords submit under MTD?

Quarterly, 4 times per tax year (deadlines: 7 August, 7 November, 7 February, 7 May) plus a Final Declaration by 31 January following the tax year end.

Are non-resident landlords affected by MTD?

Yes, if your UK rental income exceeds the threshold. The Non-Resident Landlord (NRL) Scheme is separate, but you must also comply with MTD ITSA reporting. Both apply.

What if I own property through a limited company?

Limited company landlords are subject to Corporation Tax, not ITSA. MTD for Corporation Tax is expected to begin April 2027, with similar quarterly reporting requirements.

Are holiday lets affected by MTD?

Yes, the Furnished Holiday Let (FHL) regime was abolished in April 2025. Holiday let income now counts as standard rental income for MTD threshold purposes.

Do joint property owners need to register separately for MTD?

Yes, each joint owner reports their share separately. The MTD threshold applies to each individual’s qualifying income, not the property as a whole.

What if my rental income drops below the threshold?

Once you’re in MTD ITSA, you stay in for a minimum of 3 years, even if your income drops below the threshold in subsequent years.

Can I still claim mortgage interest under MTD?

Mortgage interest is no longer a deductible expense, it’s a 20% basic-rate tax credit (Section 24 rules, unchanged by MTD). You must record the interest paid, but it doesn’t reduce taxable rental profit directly.

What is the penalty for landlords missing MTD deadlines?

Penalty points lead to a £200 fine after 4 missed quarterly submissions. Late payment penalties of 3-10% apply. Failing to keep digital records can incur fines up to £3,000.

Do I need an accountant for MTD as a landlord?

Technically no, small landlords (1-2 properties) can DIY. But landlords with portfolios, HMOs, holiday lets, joint ownership, or non-resident status almost always benefit from chartered accountant support.

Get MTD-Ready as a UK Landlord, Speak to ICAEW Chartered Specialists

UK landlords face some of the most complex Making Tax Digital changes of any taxpayer group. Multiple properties, Section 24 rules, joint ownership, NRL scheme, abolished FHL regime — the rules are layered and the penalties for getting it wrong are high.

At MTD – Making Tax Digital (part of B1 Accountants), our ICAEW chartered accountants specialise in landlord tax compliance. We help:

- Buy-to-let landlords (1-50+ property portfolios)

- HMO operators and student-let landlords

- Holiday-let and Airbnb owners

- Accidental landlords renting their former home

- Non-resident landlords living overseas

- Joint property owners (couples, family members)

Our landlord MTD service includes:

- MTD software setup with property-level tracking

- All quarterly submissions managed for you

- Year-end Final Declaration with tax optimisation

- Section 24 mortgage interest handling

- HMRC enquiry defence if needed

- Transparent monthly pricing per landlord type

Book your free 30-minute MTD consultation — no obligation. We’ll review your situation, explain exactly what MTD means for you, and give you a clear plan.

BOOK YOUR FREE MTD CLARITY CALL →

Or call us directly: +44 (0) 75 079 66252

Bilal Chudher

(FCCA, FCA, TEP & MBA) Chartered Accountant