Categories

Latest Post

Making Tax Digital Checklist 2026

MTD Quarterly Updates 2026

MTD Qualifying Income Explained 2026

Making Tax Digital Penalties 2026

Have Any Question?

If you have any questions about our services, call us or email at:

- +44 75 079 66252

- contact@mtd-makingtaxdigital.co.uk

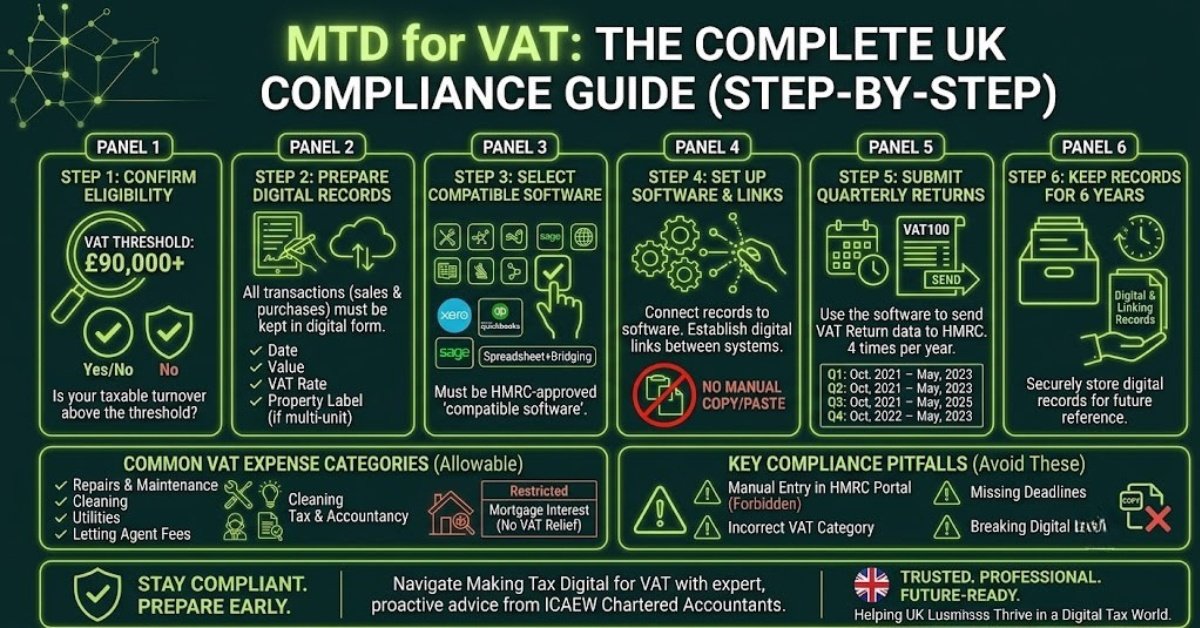

MTD for VAT: The Complete UK Compliance Guide (Step-by-Step)

Making Tax Digital for VAT (MTD for VAT) has been mandatory in the UK since April 2022 for every VAT-registered business — regardless of turnover. But here’s what most business owners don’t realise: a huge number of VAT-registered UK businesses are still using their old methods, unaware that they’re already non-compliant and exposed to HMRC penalties of up to £400 per return.

If you’re VAT-registered in the UK and still using spreadsheets without bridging software, filing through HMRC’s free online portal, or unsure whether your accounting software actually qualifies as MTD-compatible — this guide is for you.

Written by ICAEW chartered accountants who handle VAT returns for businesses across the UK every quarter, this guide covers:

- Who needs to comply with MTD for VAT

- VAT schemes and how MTD applies to each

- Approved software vs bridging software vs spreadsheets

- How to register and file step-by-step

- Deadlines, penalties, and exemptions

- How to fix non-compliance fast

Let’s start with the basics.

What Is Making Tax Digital for VAT?

Making Tax Digital for VAT (often abbreviated as MTD for VAT or VAT MTD) is HMRC’s mandatory digital VAT reporting system. It replaces the old method of filing VAT returns through HMRC’s free online portal or by post.

Under MTD for VAT, every VAT-registered UK business must:

- Keep digital VAT records in HMRC-approved software

- Submit VAT returns directly through MTD-compatible software (no manual online portal entry)

- Maintain digital links between any software/spreadsheets used (no copy-pasting)

Important: HMRC’s free VAT online filing service is no longer compliant for MTD businesses. If you’re still entering VAT return numbers manually into the HMRC website, you’re filing through a non-compliant route and exposed to penalties.

Who Must Comply with MTD for VAT in the UK?

Since 1 April 2022, MTD for VAT applies to ALL VAT-registered businesses in the UK, regardless of turnover. There’s no minimum threshold for MTD VAT once you’re VAT-registered.

MTD for VAT Applies If You’re:

Above the VAT threshold — turnover over £90,000 (2024+) and compulsorily registered

Voluntarily VAT-registered — below £90k but chose to register

Trading as a limited company — with VAT registration

Trading as a sole trader — with VAT registration

Trading as a partnership — with VAT registration

Operating special VAT schemes — Flat Rate, Cash Accounting, Annual Accounting, Margin scheme

MTD for VAT Does NOT Apply If You’re:

Not VAT-registered at all

Below the VAT threshold AND not voluntarily registered

Granted a specific HMRC digital exclusion exemption (rare — religious grounds, severe disability, remote location)

Reality check: If you’re VAT-registered in 2026 and still using the HMRC online portal manually or filing without compatible software, HMRC can fine you £400 per return. Many businesses are unknowingly in this position.

UK VAT Registration Threshold 2026 (And How MTD Fits In)

Here are the current UK VAT thresholds:

Threshold Type | Amount (2026) | What It Means |

|---|---|---|

Mandatory VAT registration | £90,000 turnover (12-month rolling) | Must register within 30 days of exceeding |

Voluntary VAT registration | Any turnover | Can register below threshold for input VAT recovery |

De-registration threshold | £88,000 turnover | Can de-register if turnover falls below |

MTD VAT applies | All VAT-registered (£0+) | No minimum — applies once registered |

The MTD threshold is separate from the VAT threshold. Once you’re VAT-registered (voluntarily or mandatorily), MTD applies in full.

MTD for VAT by Scheme: Standard, Flat Rate, Cash Accounting & More

UK businesses use different VAT schemes depending on their size, sector, and cash flow needs. MTD applies to all of them — but the rules differ slightly:

1. Standard VAT Accounting Scheme

The most common scheme. Used by businesses with turnover above £1.35 million (mandatory) or any business that chooses to use it. Under MTD:

Submit quarterly VAT returns digitally via approved software

Maintain digital records of all sales (output VAT) and purchases (input VAT)

Account for VAT on invoices issued, not when paid

2. Cash Accounting Scheme

For businesses with turnover under £1.35 million. You account for VAT when cash actually moves — not when invoices are issued. Under MTD:

Same quarterly digital submissions required

Digital records must track payment dates, not just invoice dates

Useful for businesses with slow-paying customers

3. Flat Rate Scheme (FRS)

For businesses with turnover under £150,000. You pay a fixed percentage of gross turnover instead of standard VAT calculations. Under MTD:

Still submit quarterly digital returns

Digital records of total sales required

Limited input VAT reclaim (only on capital assets over £2,000)

Simpler bookkeeping but check if it’s actually saving you money

4. Annual Accounting Scheme

For businesses with turnover under £1.35 million. Submit ONE VAT return per year instead of four. Under MTD:

Single annual digital VAT return

Monthly or quarterly advance payments based on previous year

Useful for businesses with predictable cash flow

5. Margin Schemes (Second-Hand Goods, Antiques, Art, Cars)

VAT calculated on the margin (selling price minus purchase price). Under MTD:

Specialist digital record-keeping required

Each item tracked separately

Used by dealers in second-hand goods, antiques, art, classic cars

Choosing the right VAT scheme can save you thousands per year — but most businesses pick the wrong one. As chartered accountants, we review every client’s VAT setup annually to ensure they’re on the most tax-efficient scheme.

MTD for VAT Deadlines & Filing Frequency

Most UK VAT-registered businesses file quarterly, though monthly and annual schemes also exist. Your specific VAT periods are set by HMRC when you register.

Standard Quarterly VAT Deadlines

VAT Period | VAT Return & Payment Deadline |

|---|---|

January – March (Q1) | 7 May |

April – June (Q2) | 7 August |

July – September (Q3) | 7 November |

October – December (Q4) | 7 February |

Your VAT periods might not align with calendar quarters — HMRC assigns them when you register. Check your Government Gateway account or speak to a chartered accountant if you’re unsure.

Monthly VAT Filing

Some businesses opt for monthly returns (typically those expecting regular VAT refunds, like exporters or input-heavy startups). Monthly deadlines are 1 month + 7 days after the period ends.

Annual VAT Filing

If you’re on the Annual Accounting Scheme, your single annual return is due 2 months after your VAT year-end. Advance payments are made monthly or quarterly throughout the year.

Critical: VAT return AND payment are both due on the same deadline. Late payment incurs separate penalties on top of late filing — making it one of the most expensive errors a VAT business can make.

See our complete MTD Deadlines & Key Dates guide for every UK tax deadline through 2028.

Best MTD-Compatible Software for UK VAT Returns

To comply with MTD for VAT, you must use HMRC-approved software. Here are the most popular options used by UK businesses:

Full Accounting Software (Recommended for Most Businesses)

Software | Best For | Approx Cost |

|---|---|---|

Xero | SMEs, growing businesses, multi-user teams | £15-£40/month |

QuickBooks Online | Sole traders, freelancers, small Ltd Cos | £10-£30/month |

Sage Business Cloud | Established UK SMEs, larger businesses | £14-£40/month |

FreeAgent | NatWest/RBS account holders, sole traders | Free or £15/month |

Zoho Books | Budget-conscious businesses | £10-£25/month |

IRIS Kashflow | UK-focused, accountant-friendly | £15-£30/month |

Bridging Software (If You Still Use Excel)

If you maintain your VAT records in Excel and don’t want to switch to full accounting software, you can use bridging software to submit MTD-compliant returns from your spreadsheet.

Bridging Software | Notes | Approx Cost |

|---|---|---|

123Sheets | Most popular UK bridging tool, simple | £12-£24/year |

VitalTax (Excel add-in) | Built into Excel, easy to use | Free (basic) / £40+/year |

Bx by AccountancyManager | For accountancy practices | Practice-only |

Easy MTD VAT | Standalone, low-cost bridging app | £10-£25/year |

MTD Vat Bridge | Lightweight, single-user | £0-£15/year |

Bridging software vs full accounting software — when to choose which: If you only need to file MTD VAT and your records are already clean in Excel, bridging software is fine. If you want better cash flow visibility, automated invoicing, expense tracking, and easier MTD ITSA prep (coming in 2026), full accounting software is the better long-term investment.

See our complete software comparison: Best MTD Software UK 2026 and our MTD Spreadsheets & Bridging Software guide.

The Digital Links Rule (Most Businesses Miss This)

Under MTD for VAT, data must transfer digitally between any software you use — no copying and pasting. This is one of the strictest MTD rules and the one most businesses unknowingly break.

✅ Acceptable Digital Links:

- Excel formula references (=A1+B1 etc.)

- API connections between software

- CSV imports/exports between systems

- XML transfers

- Linked cells between Excel sheets/workbooks

- Email of CSV files between systems (yes, this counts)

❌ NOT Acceptable (= Non-Compliant):

- Copy and pasting numbers between spreadsheets

- Manually typing figures from one system into another

- Hand-writing notes to enter into software later

- Re-keying VAT totals into the HMRC online portal

The £3,000 penalty: HMRC can fine businesses up to £3,000 PER FAILURE to maintain digital links. Many businesses unknowingly fail this rule by copy-pasting between their CRM, invoicing software, and VAT bridging tool.

How to Register for MTD for VAT (Step-by-Step)

If you’re newly VAT-registered or migrating from old non-MTD methods, here’s the exact process:

Step 1: Set Up MTD-Compatible Software

Choose your software (Xero, QuickBooks, Sage, etc.) and complete the initial setup BEFORE registering with HMRC for MTD.

Step 2: Sign In to Your HMRC Government Gateway

Use your business’s Government Gateway account (the one tied to your VAT registration). If you don’t have one, create it via gov.uk.

Step 3: Sign Up for MTD VAT

Visit gov.uk/guidance/sign-up-for-making-tax-digital-for-vat and follow the prompts. You’ll need:

- Your VAT number

- Business name and address

- Latest VAT return details

Step 4: Connect Your Software to HMRC

In your accounting software (Xero, QuickBooks, etc.), there’s an option to “Connect to HMRC for MTD VAT.” This authorises the software to file on your behalf.

Step 5: File Your First MTD VAT Return

Once connected, your software will pull VAT return data from your records, allow review, and submit directly to HMRC. Confirmation arrives via the software.

Pro tip: Don’t wait until your next VAT return deadline to register. The MTD signup process can take 2-3 business days for HMRC to confirm. Register at least 7 days before your filing deadline.

Read our step-by-step MTD registration guide for the full process.

MTD for VAT Penalties: What HMRC Can Fine You

HMRC has set up a tougher penalty regime specifically for VAT compliance. Here’s what you risk:

Failure | Penalty |

|---|---|

Missing quarterly VAT submission (1 quarter) | 1 penalty point (£200 fine at 4 points) |

Late VAT payment 16-30 days | 3% of VAT owed (rising to 4% from April 2027) |

Late VAT payment 31+ days | Additional 3% + 10% annual interest |

Filing through non-compatible software | £400 per non-compliant return |

Failing to keep digital VAT records | Up to £3,000 per failure |

No digital links between systems | Up to £3,000 per failure |

Misleading or fraudulent VAT claim | Up to 100% of tax owed + criminal charges |

Example: A small VAT-registered business that misses 4 quarterly returns and pays VAT 31 days late could face £200 fine + £400 x 4 (non-compatible software) + £600 in late payment penalties = over £2,200 in penalties on top of the VAT owed.

Read the full MTD Penalties guide for every penalty scenario.

MTD for VAT Exemptions: Who Can Opt Out?

HMRC grants very limited exemptions from MTD for VAT. You can apply for an exemption if you can prove that you cannot use digital tools due to:

- Age or disability — preventing use of computers or software

- Religious grounds — certain religious denominations restricting electronic communications

- Remoteness of location — no reliable internet access in your area

- Insolvency — if your business is in formal insolvency proceedings

You must apply for exemption in writing to HMRC and provide evidence. Approval is not automatic and is rare — HMRC’s default position is that all VAT-registered businesses must comply.

Read our full MTD Exemptions guide for the application process.

5 Biggest MTD for VAT Mistakes (And How to Fix Them)

Mistake 1: Still Filing Through HMRC’s Online Portal

Many VAT-registered businesses haven’t realised the old online portal is no longer MTD-compliant. If you’re typing VAT figures directly into HMRC’s website, you’re filing through a non-compliant route and exposed to £400/return penalties.

Fix: Switch to MTD-compatible software immediately. Connect it to HMRC and file from within the software.

Mistake 2: Copy-Pasting Between Excel and Software

Even if you use MTD software for filing, copy-pasting from spreadsheets, CRMs, or invoicing tools breaks the digital links rule.

Fix: Use formula links, API connections, or CSV imports/exports between all your data sources.

Mistake 3: Wrong VAT Scheme

Many businesses are on the wrong VAT scheme — paying more VAT than necessary. The Flat Rate Scheme might suit a service business but cost a retailer thousands more per year.

Fix: Review your VAT scheme annually with a chartered accountant. Switching can save thousands.

Mistake 4: Not Reclaiming Input VAT on Pre-Registration Expenses

Many businesses miss claimable input VAT on expenses incurred BEFORE VAT registration (up to 4 years for goods, 6 months for services). This is a common oversight.

Fix: Audit your pre-registration expenses with your accountant on the first VAT return.

Mistake 5: Ignoring Reverse Charge VAT

If you buy services from EU or non-UK suppliers (e.g., Facebook Ads, Google Ads, AWS), the reverse charge mechanism applies. You must account for VAT on these — but many businesses don’t.

Fix: Set up reverse charge VAT codes in your software. Get expert advice if unsure.

Real Case Study: How We Defended a VAT Investigation

An import/export clothing and fashion retailer came to us facing a full HMRC enquiry into their last 4 quarters of VAT returns. HMRC was questioning every input VAT reclaim, suggesting potential disallowances totalling tens of thousands.

What we did:

- Compiled all supporting invoices, supplier agreements, and shipping documentation

- Built detailed VAT calculation assessments for every disputed reclaim

- Cross-referenced HMRC’s challenge with VAT law and case precedents

- Presented a structured defence to HMRC’s enquiry team

- Negotiated with HMRC to resolve outstanding queries

Outcome: Enquiry resolved with all VAT reclaims fully supported. No disallowances, no penalties, no clawback. Total VAT protected: significant.

Lesson: Under MTD for VAT’s quarterly visibility, HMRC’s algorithms can flag suspicious patterns much faster. Businesses with clean digital records, proper digital links, and chartered accountant support have a major defensive advantage.

MTD for VAT: Frequently Asked Questions

Who needs to use Making Tax Digital for VAT?

All VAT-registered UK businesses, regardless of turnover. Since 1 April 2022, MTD for VAT applies to every VAT-registered business — including voluntarily registered ones below the £90,000 threshold.

What is the MTD VAT threshold?

There is no minimum threshold for MTD VAT. Once you’re VAT-registered (mandatory at £90k turnover, voluntary at any turnover), MTD applies in full.

How often do I submit MTD VAT returns?

Most businesses file quarterly (4 returns per year). Some opt for monthly filing (typically exporters expecting refunds), or annual filing (under the Annual Accounting Scheme).

What software is approved for MTD for VAT?

HMRC maintains a list of approved software at gov.uk. Popular options include Xero, QuickBooks, Sage, FreeAgent, Zoho Books, IRIS Kashflow, and bridging tools like 123Sheets, VitalTax, and Easy MTD VAT.

Can I still use Excel for MTD VAT?

Yes — but only with HMRC-approved bridging software (123Sheets, VitalTax, etc.) that submits your Excel-based VAT data digitally to HMRC. Sending raw spreadsheets is not compliant.

What is the digital links rule?

Data must transfer digitally between any software/spreadsheets you use for VAT records. Copy-pasting numbers between systems is non-compliant. Use formula links, API connections, or CSV imports.

What happens if I miss a VAT return deadline?

You’ll receive 1 penalty point. Accruing 4 points (for quarterly filers) triggers a £200 fine. Late payment of VAT also incurs penalties of 3-10% depending on how late you pay.

Can I file MTD VAT returns myself or do I need an accountant?

You can file MTD VAT yourself if you have approved software and clean digital records. However, businesses with complex VAT (reverse charge, partial exemption, margin schemes, mixed-rate sales) usually benefit significantly from chartered accountant support.

What is the VAT registration threshold for 2026?

£90,000 in turnover over a rolling 12-month period (mandatory). You must register within 30 days of exceeding the threshold. Voluntary registration is available at any turnover.

Are charities and non-profits subject to MTD for VAT?

If a charity or non-profit is VAT-registered (some are, depending on their activities), then yes — MTD for VAT applies. Charity-specific VAT rules still apply alongside MTD.

How do I change my VAT scheme (e.g., from Standard to Flat Rate)?

You can apply to change schemes via your Government Gateway account or by writing to HMRC. Each scheme has its own qualifying criteria — speak to a chartered accountant before switching.

What if I’m VAT-registered but my turnover drops below £88,000?

You can apply to de-register from VAT (the de-registration threshold is £88,000). However, this might not be tax-efficient if you reclaim significant input VAT. Get advice before de-registering.

Do I need MTD VAT if I’m on the Annual Accounting Scheme?

Yes — MTD applies to all VAT schemes. Under Annual Accounting, you submit one digital return per year (instead of quarterly), with advance payments throughout the year.

Can I get an exemption from MTD for VAT?

Exemptions are granted only on very narrow grounds: age/disability preventing computer use, religious grounds, lack of internet in your area, or formal insolvency. You must apply in writing to HMRC with evidence.

What’s the difference between MTD for VAT and MTD for Income Tax?

MTD for VAT applies to VAT-registered businesses (already mandatory since 2022). MTD for Income Tax Self-Assessment (ITSA) applies to landlords and self-employed individuals starting April 2026 — a different system covering income tax, not VAT.

Get Your MTD VAT Compliance Right – Speak to ICAEW Chartered Specialists

MTD for VAT has been mandatory since 2022 — but many UK VAT-registered businesses are still non-compliant without realising it. Wrong software, broken digital links, manual portal filing, missed reclaims — every one of these exposes your business to HMRC penalties of £400 to £3,000+ per failure.

At MTD – Making Tax Digital (part of B1 Accountants), our ICAEW chartered accountants specialise in VAT compliance for UK businesses. We handle:

- Full MTD VAT setup and migration from non-compliant systems

- Quarterly VAT returns prepared, reviewed, and filed for you

- VAT scheme review and optimisation (Standard, Flat Rate, Cash, Annual, Margin)

- Input VAT reclaim audits to ensure you’re claiming everything

- Reverse charge VAT handling for international purchases

- HMRC VAT enquiry defence and dispute resolution

- Transparent monthly pricing — no surprise fees

Book your free 30-minute VAT MTD consultation — we’ll review your current setup, identify compliance gaps, and give you a clear plan.

Book your free 30-minute MTD consultation — no obligation. We’ll review your situation, explain exactly what MTD means for you, and give you a clear plan.

BOOK YOUR FREE MTD CLARITY CALL →

Or call us directly: +44 (0) 75 079 66252

Bilal Chudher

(FCCA, FCA, TEP & MBA) Chartered Accountant