Making Tax Digital Thresholds Explained (£50k, £30k, £20k Limits)

Whether or not Making Tax Digital (MTD) applies to you depends on one number: your qualifying income. If you’re a self-employed person or landlord in the UK, knowing exactly where you sit against the MTD thresholds is the difference between being prepared by April 2026, or being hit with HMRC penalties starting at £200.

This guide explains every Making Tax Digital threshold, when each applies, what counts as qualifying income, and exactly how to check whether you’re in scope right now. Written by ICAEW chartered accountants who advise UK taxpayers on these exact rules.

Let’s start with the headline numbers.

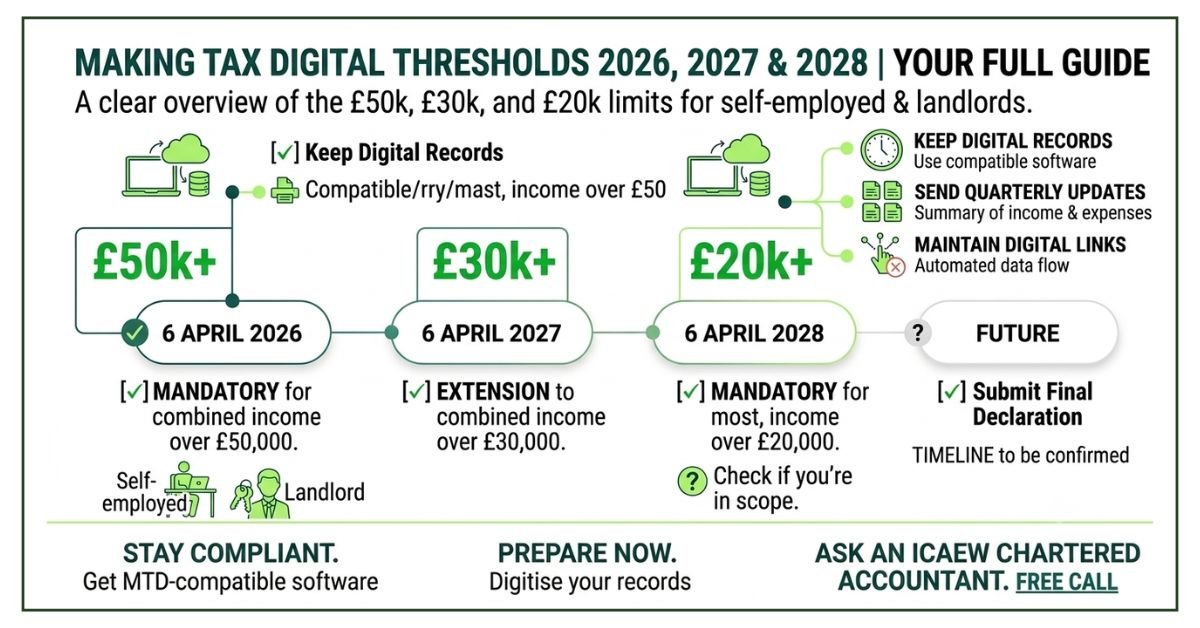

MTD Thresholds at a Glance: 2026, 2027, 2028

HMRC is rolling out MTD for Income Tax Self-Assessment (ITSA) in 3 phases — each with a lower income threshold:

Tax Year Starting | Threshold | Phase |

|---|

6 April 2026 | Over £50,000 | Phase 1 — Higher earners |

6 April 2027 | Over £30,000 | Phase 2 — Mid-tier |

6 April 2028 | Over £20,000 | Phase 3 — Most UK self-employed and landlords |

Critical rule: Once you exceed the threshold and enter MTD ITSA, you stay in for a MINIMUM of 3 years, even if your income drops below the threshold in subsequent years. The threshold check is at entry, not yearly.

What Income Counts Toward the MTD Threshold?

HMRC uses qualifying income, this is your gross income (before expenses), NOT your taxable profit.

Counts Toward MTD Threshold:

Self-employment turnover (gross sales/revenue)

UK property rental income (gross rent received)

Overseas property rental income (if you’re UK-resident)

Income from furnished holiday lets / Airbnb

Service charges or licence fees received from tenants

Income from licensing rooms (e.g., HMO landlords)

Does NOT Count Toward MTD Threshold:

PAYE salary or employment income

Dividends (from your own company or shares)

Interest income (savings, bonds)

Pension income (state, private, or workplace)

Capital gains (from property sales, share sales, etc.)

Investment income from ISAs

Income below the £1,000 trading allowance

Rent-a-Room income below £7,500/year

Most common misunderstanding: People assume the threshold is based on profit. It’s NOT, it’s based on gross income. A landlord with £42,000 in rent and £30,000 in expenses (so £12,000 profit) still has £42,000 of qualifying income.

MTD Thresholds by Audience

MTD Self-Employed Threshold

If you’re self-employed (sole trader, freelancer, gig worker, side hustler), the MTD threshold is based on your gross self-employment turnover plus any property income.

Tax Year | Self-Employed Threshold | Action |

|---|

April 2026 | £50,000+ qualifying income | Register for MTD ITSA by March 2026 |

April 2027 | £30,000+ qualifying income | Register by March 2027 |

April 2028 | £20,000+ qualifying income | Register by March 2028 |

Read our full MTD for Self-Employed guide for details.

MTD Landlord Threshold

If you’re a UK landlord, the threshold is based on gross rental income (before mortgage interest, maintenance, and other expenses) combined with any self-employment income.

Tax Year | Landlord Threshold | Action |

|---|

April 2026 | £50,000+ gross rent + self-employment | Register for MTD ITSA by March 2026 |

April 2027 | £30,000+ qualifying income | Register by March 2027 |

April 2028 | £20,000+ qualifying income | Register by March 2028 |

Landlord specific: If you own property jointly, each owner’s share of the rental income is calculated separately. The threshold applies to each individual’s qualifying income, not the property as a whole.

Read our complete MTD for Landlords guide for landlord-specific scenarios.

MTD ITSA Threshold (Combined Income)

If you have both self-employment AND property income, they are added together to check the MTD ITSA threshold:

Self-Employment Income | + Property Income | = Qualifying Income | MTD ITSA Status |

|---|

£35,000 | £20,000 | £55,000 | ✅ April 2026 |

£25,000 | £10,000 | £35,000 | ✅ April 2027 |

£15,000 | £8,000 | £23,000 | ✅ April 2028 |

£18,000 | £0 | £18,000 | ❌ Under all thresholds |

£45,000 | £0 | £45,000 | ✅ April 2027 |

MTD VAT Threshold

MTD for VAT is separate from MTD ITSA and operates differently:

- MTD for VAT applies to ALL VAT-registered businesses (since April 2022)

- There is NO minimum threshold for MTD VAT — once you’re VAT-registered, MTD applies

- VAT registration is mandatory at £90,000 turnover (2024+ figure)

- Voluntary VAT registration is available at any turnover

Read our complete MTD for VAT guide for full details.

How to Calculate Your MTD Threshold Income (Step-by-Step)

Use this 5-step method to check if you’re in scope:

Step 1: Add Up Your Self-Employment Turnover

Total the gross sales/revenue from your self-employment for the past 12 months. This is the figure BEFORE deducting any business expenses.

Example: If you’re a freelance designer who invoiced £42,000 across the year (even if you only kept £30,000 after expenses), your self-employment qualifying income is £42,000.

Step 2: Add Your Gross Rental Income

Add all rental income you received from UK and overseas property in the past 12 months. Use gross rent (before mortgage interest, maintenance, agent fees, etc.).

Example: If you own a flat in Birmingham with £12,000 annual rent and a house in Manchester with £18,000 annual rent, your rental qualifying income is £30,000.

Step 3: Combine the Two

Total qualifying income = Self-employment turnover + Gross rental income

In our example: £42,000 (freelance) + £30,000 (rent) = £72,000 total qualifying income.

Step 4: Compare Against the Threshold

If Your Qualifying Income Is… | Then… |

|---|

Over £50,000 | ✅ In scope from April 2026 |

£30,000 – £50,000 | ✅ In scope from April 2027 |

£20,000 – £30,000 | ✅ In scope from April 2028 |

Under £20,000 | ❌ Not in scope (yet — thresholds may drop further) |

Step 5: Note Your Earliest Threshold Date

If you’re in scope, the date you must be MTD-ready is 6 April of that tax year. Start preparing at least 6 months in advance.

Quick tip: HMRC determines your in-scope status based on your last filed tax return. So even if your income drops this year, you may still be in scope based on prior years’ figures.

Real Worked Examples (UK Taxpayers)

Example 1: Sarah, Freelance Web Designer

Income Source | Annual Amount | Counts? |

|---|

Freelance web design | £48,000 |  Yes Yes

|

Rental income from one flat | £8,000 | Yes |

PAYE salary (part-time) | £12,000 |  No No

|

TOTAL QUALIFYING INCOME | £56,000 | In scope April 2026 |

Sarah is in scope from April 2026 because her combined freelance + rental income (£56k) exceeds the £50k threshold. Her PAYE salary is excluded.

Example 2: Mike, Plumber (Sole Trader)

Income Source | Annual Amount | Counts? |

|---|

Plumbing business turnover | £42,000 | Yes |

Side income — emergency callouts | £3,500 | Yes |

No rental income | £0 | — |

TOTAL QUALIFYING INCOME | £45,500 | In scope April 2027 |

Mike is under the £50k April 2026 threshold but over the £30k April 2027 threshold. He has until March 2027 to be ready.

Example 3: Priya, Etsy Seller + PAYE Employee

Income Source | Annual Amount | Counts? |

|---|

Etsy crafts business | £18,500 | Yes |

PAYE salary (admin job) | £28,000 | No |

Dividend from ISA | £600 | No |

TOTAL QUALIFYING INCOME | £18,500 | Not in scope (yet) |

Priya is currently not in MTD scope because her Etsy income is under £20k. However, if her Etsy business grows above £20k, she’ll be in scope from April 2028.

Example 4: James, Multi-Property Landlord

Income Source | Annual Amount | Counts? |

|---|

4 BTL properties (gross rent) | £62,000 | Yes |

1 HMO (5 tenants) | £24,000 | Yes |

PAYE full-time job | £42,000 | No |

TOTAL QUALIFYING INCOME | £86,000 | In scope April 2026 |

James is firmly in scope from April 2026 with £86k of qualifying rental income. His PAYE salary doesn’t count toward the threshold.

Example 5: Tom, Joint Property Owner (with Spouse)

Property | Gross Rent | Tom’s Share (50%) | Spouse’s Share (50%) |

|---|

Property 1 (joint) | £24,000 | £12,000 | £12,000 |

Property 2 (joint) | £18,000 | £9,000 | £9,000 |

Property 3 (joint) | £15,000 | £7,500 | £7,500 |

TOTAL | £57,000 | £28,500 | £28,500 |

Tom and his spouse own all 3 properties jointly. Each individual has £28,500 qualifying income. Both are in scope from April 2028 (under £30k threshold). Smart tax planning — combined, the income would have been over £50k.

Common Threshold Confusions Explained

Confusion 1: “Is the threshold based on profit or revenue?”

Revenue / turnover (gross), not profit. Even if your profit after expenses is much lower than your turnover, HMRC uses the gross figure to check the threshold.

Confusion 2: “Does my PAYE salary count?”

No. PAYE employment income is completely excluded from the MTD qualifying income calculation. Only self-employment and property income count.

Confusion 3: “What if my income fluctuates year to year?”

HMRC checks your last submitted self-assessment to determine if MTD applies. If your income spikes in 2024-25 and drops in 2025-26, HMRC may still consider you in scope based on the higher year. Once you’re in MTD ITSA, you stay in for a minimum of 3 years.

Confusion 4: “What if I’m under the threshold but registered voluntarily for VAT?”

Different systems. MTD for VAT applies once you’re VAT-registered (no minimum threshold for MTD VAT). MTD ITSA is separate and based on the qualifying income threshold (£50k/£30k/£20k).

Confusion 5: “Do limited company directors need to worry about the MTD threshold?”

Not for MTD ITSA. Limited company income falls under Corporation Tax, not Income Tax Self-Assessment. MTD for Corporation Tax is expected from April 2027 with similar quarterly requirements. However, if you also have personal self-employment or rental income, that still counts toward the MTD ITSA threshold.

What to Do If You’re in Scope (By Threshold)

If You’re in Scope from April 2026 (Over £50,000)

- Start preparing NOW — less than 6 months until live

- Choose MTD-compatible software (Xero, QuickBooks, FreeAgent, etc.)

- Register with HMRC via Government Gateway

- Open a separate business bank account if you haven’t already

- Consider hiring a chartered accountant for ongoing support

If You’re in Scope from April 2027 (£30,000 – £50,000)

- You have ~18 months — start preparing now to avoid the April 2027 rush

- Trial MTD software with current data

- Build digital record-keeping habits

If You’re in Scope from April 2028 (£20,000 – £30,000)

- Use 2025-26 and 2026-27 to learn and prepare

- Set up MTD software voluntarily

- Plan for the £20k threshold (covers almost all UK self-employed)

If You’re Currently Under £20,000

- Not in scope (yet) — but threshold may drop further

- HMRC has signalled possible future expansion of MTD

- Voluntary digital record-keeping now will make any future transition easier

Download our free MTD Checklist (printable PDF) to track your progress.

MTD Thresholds: Frequently Asked Questions

What is the threshold for Making Tax Digital?

The MTD ITSA threshold is £50,000 of qualifying income from April 2026, dropping to £30,000 in April 2027 and £20,000 in April 2028. Qualifying income includes gross self-employment turnover plus gross rental income.

What is the MTD income threshold?

The MTD income threshold for income tax (MTD ITSA) is £50,000 of gross qualifying income from April 2026. It will drop to £30,000 from April 2027 and £20,000 from April 2028.

Is the MTD threshold based on profit or turnover?

Gross turnover/revenue, NOT profit. HMRC uses your gross self-employment and rental income (before deducting expenses) to determine if you’re in scope.

What is the MTD self-employed threshold?

Same as the general MTD ITSA threshold: £50,000 from April 2026, £30,000 from April 2027, £20,000 from April 2028. Based on gross self-employment turnover plus any rental income.

What is the MTD threshold for landlords?

Same as the general MTD ITSA threshold: £50,000 of gross rental income (plus any self-employment) from April 2026, dropping to £30,000 in 2027 and £20,000 in 2028.

Does PAYE salary count toward the MTD threshold?

No. PAYE employment income is excluded from MTD qualifying income calculations. Only self-employment turnover and gross rental income count.

What is the MTD VAT threshold?

There is NO threshold for MTD VAT — it applies to all VAT-registered businesses, regardless of turnover. The VAT registration threshold itself is £90,000 of taxable turnover for mandatory registration.

Does the MTD threshold include overseas income?

Overseas property rental income counts if you’re a UK tax resident. Overseas self-employment income may also count depending on how it’s structured — get specialist advice if applicable.

What happens if my income drops below the MTD threshold?

Once you’re in MTD ITSA, you stay in for a minimum of 3 years — even if your income drops below the threshold in subsequent years.

Do joint property owners need to combine income for the threshold?

No. Each joint owner reports their share separately. The threshold applies to each individual’s qualifying income.

What is the MTD ITSA threshold?

MTD ITSA stands for Making Tax Digital for Income Tax Self-Assessment. The threshold is £50,000 of qualifying income from April 2026, dropping to £30,000 (April 2027) and £20,000 (April 2028).

Will the MTD threshold drop below £20,000 in future?

Possibly — HMRC has signalled potential future expansion. Treasury reviews are ongoing. Currently confirmed thresholds end at £20,000 from April 2028.

What if I have multiple income streams below each individual threshold?

Combine them. If your total qualifying income (self-employment + property) exceeds the threshold, you’re in scope — even if each individual stream is under £50k/£30k/£20k.

How does HMRC know if I’m in scope for MTD?

HMRC uses your last submitted self-assessment tax return to identify in-scope taxpayers. They’ve been sending letters since 2024 to those they expect to qualify.

Can I voluntarily opt into MTD before reaching the threshold?

Yes. HMRC has a voluntary opt-in pilot allowing taxpayers below the threshold to join MTD ITSA early. This can be useful for tax planning.

Not Sure Where You Sit Against the MTD Thresholds? Let Us Check for You

If you’re unsure whether your income puts you in scope for MTD ITSA — or which tax year you need to be ready for — get clarity from chartered accountants who handle these calculations daily.

At MTD – Making Tax Digital (part of B1 Accountants), our ICAEW chartered accountants offer:

- Free MTD threshold assessment — we calculate your exact status

- Clear explanation of which tax year you must be ready for

- Action plan tailored to your situation

- Full MTD setup and ongoing support if needed

- Tax planning advice to optimise your position

BOOK YOUR FREE THRESHOLD CHECK →

BOOK YOUR FREE THRESHOLD CHECK →